Should You Claim Social Security at 62, 67, or 70? Plain-English Math for Pre-Retirees

It might be the most expensive button you ever push.

Once you tell Social Security when to start your benefit, that decision locks in for the rest of your life. There's a narrow 12-month window to undo it, but for most retirees the choice is permanent — and depending on which doorway you walk through, the difference can add up to six figures over a long retirement.

So let's slow down and walk through it together, the way I'd talk it over with a friend at the kitchen table.

The three doorways

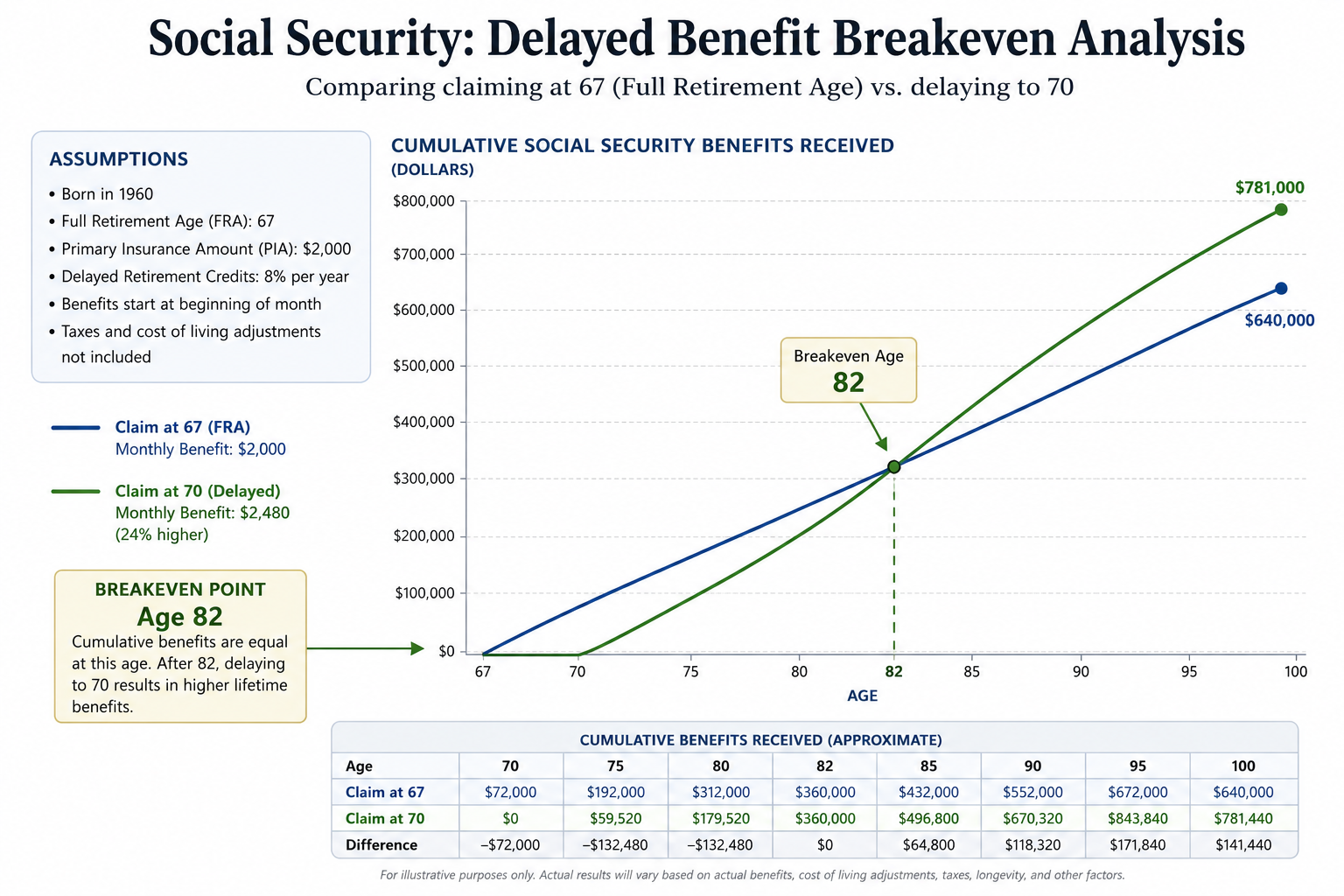

For anyone born in 1960 or later — which covers nearly everyone reading this — your full retirement age (Social Security's term for "100% of what you earned") is 67. You can claim earlier or later, but those choices come with built-in discounts and bonuses.

Here's what those choices look like in real numbers. Say your full benefit at age 67 would be $2,500 a month — close to the average for higher earners today.

Claim at 62: Your check is cut by 30%. That $2,500 becomes about $1,750 a month — for life.

Claim at 67: You get your full benefit — $2,500 a month.

Claim at 70: You get a 24% raise. That $2,500 becomes $3,100 a month — for life, adjusted for inflation every year.

The difference between claiming at 62 and waiting until 70 is roughly $1,350 a month, or $16,200 a year, every year for the rest of your life. Compound that over a 25-year retirement and you're looking at potentially $400,000 or more in lifetime benefits — even before factoring in cost-of-living adjustments.

The 8% raise nobody talks about

Between full retirement age and 70, Social Security gives you a guaranteed 8% bump in your benefit for every year you wait. Not 8% on your portfolio — 8% on your lifetime monthly check.

Try finding that anywhere else. CDs, bonds, even a well-diversified stock portfolio — none of them offer a guaranteed 8% with no market risk and a built-in inflation hedge. This is one of the most generous deals the federal government still hands out, and many people give it back by claiming too early.

So why doesn't everyone wait?

Because life is more complicated than a calculator.

You'll often hear about the "break-even age" — the point where the bigger checks you get from waiting catch up to all those smaller checks you skipped. The break-even between claiming at 62 versus 67 lands around age 79. The break-even between 67 and 70 lands closer to 82.

Translation: if you live past your early 80s, waiting paid off. If you don't, claiming earlier put more total dollars in your pocket.

But here's why I think break-even math gets too much airtime. Social Security isn't a math problem you're trying to "win." It's longevity insurance. The real question isn't "how do I squeeze out the most total dollars?" It's "how do I make sure I don't run out of money if I live a long time?" And on that question, waiting is almost always the right answer.

When claiming early actually makes sense

I'm not in the camp that says everyone should wait until 70. Sometimes claiming at 62 is the right call. A few honest reasons:

Your health. If you have a serious condition or a strong family history of shorter lifespans, claiming earlier may genuinely put more in your pocket.

You need the income now. If you've been forced into early retirement and have no other reasonable income, the bird in hand wins.

You want investments to grow. Some people claim early so they can leave a 401(k) untouched longer. The math here is trickier than it sounds — usually waiting still wins — but it's worth running the numbers.

You're still working. Heads up: if you claim before full retirement age and keep working, Social Security claws back $1 in benefits for every $2 you earn over $24,480 in 2026. That's not lost forever — you'll get it back later — but it can be a nasty surprise.

When waiting wins

Waiting tends to win when:

You expect to live past 82 — and most healthy 65-year-olds do.

You're the higher earner in a couple. Your benefit becomes the survivor benefit for whichever spouse lives longest, so maximizing it is one of the most powerful things you can do for a surviving spouse — especially given that women on average outlive men by several years.

You have other income between retirement and 70: a pension, a Roth IRA, taxable savings, or part-time work that can comfortably bridge the gap.

You're worried about inflation eating your savings. Social Security comes with automatic cost-of-living adjustments. Most other income sources don't.

The question I really wish people would ask

Most people ask: "When should I claim?"

The better question is: "If I live to 90, will I be glad I made this choice?"

Reframing it that way usually clarifies things fast.

Three questions to ask yourself

What's my realistic life expectancy? Look at your own health honestly, and look at your parents and grandparents. The Social Security Administration has free life-expectancy calculators that are a useful starting point.

What's my income picture between 65 and 70? If you can comfortably bridge those years from savings, a pension, or part-time work, delaying becomes easier.

Am I the higher earner, and is my spouse younger and healthier than I am? If so, your delayed benefit may be the most important financial gift you ever leave behind.

One more thing

This isn't a decision you have to make alone, and it's not one to make on the fly when you turn 62. Ideally you start mapping it out in your late 50s, alongside your tax plan, your Medicare plan, and your withdrawal strategy. They're all connected.

If you'd like a second set of eyes on your own situation, I'm always happy to sit down for a no-obligation conversation. Sometimes the best thing about working with a fiduciary is just having someone in your corner who isn't trying to sell you anything — only trying to make sure you don't leave money on the table.

— Adam Elesie, Certified Financial Fiduciary®

Disclosure This article is for educational purposes only and does not constitute investment, tax, or legal advice. It should not be used as a replacement for consulting with qualified professionals in accounting, tax, legal, or financial fields. Social Security rules, benefit amounts, and tax thresholds change periodically; figures cited reflect 2026 rules and are subject to change. Examples are illustrative only — your personal results will depend on your earnings history, age, marital status, and other factors. Always confirm your specific benefit estimates with the Social Security Administration (ssa.gov) before making a claiming decision.