The Medicare Premium Surprise Most Pre-Retirees Don't See Coming

Imagine this: you've worked for decades, saved carefully, and finally handed in your badge. Medicare kicks in at 65, and you're feeling good about your plan. Then the first bill arrives — and it's $200 or $300 more per month than the standard premium you'd been counting on.

No mistake. No glitch. Just a rule that most people have never heard of, quietly doing exactly what it was designed to do.

That rule has a name: IRMAA — the Income-Related Monthly Adjustment Amount. And if you're between 55 and 65, understanding it now could save you thousands of dollars and a very unpleasant surprise.

What Is IRMAA, in Plain English?

Medicare Part B (the part that covers doctor visits and outpatient care) has a standard monthly premium. In 2026, that's $202.90 per month. Most people pay exactly that.

But if your income was above a certain threshold, Medicare charges you more — a surcharge stacked on top of that base premium. That extra charge is IRMAA.

The same thing applies to Medicare Part D (prescription drug coverage). Higher income, higher premiums.

Here's the part that trips people up: Medicare doesn't look at what you're earning right now. It looks at your income from two years ago.

The Two-Year Lookback: Why the Timing Matters So Much

Medicare uses your Modified Adjusted Gross Income (MAGI) from your federal tax return — but not last year's return. Two years back.

In 2026, your Medicare premiums are based on your 2024 income.

Why does that matter? Because many people have their highest-earning years right before they retire. A strong final salary. A year-end bonus. Severance pay. Stock options that finally vested. The sale of a business or investment property.

All of that shows up on your 2024 tax return. And Medicare sees it — even if 2026 looks very different financially.

You could be living on a modest $55,000 a year in retirement and still paying an IRMAA surcharge because your last full year of work pushed your income over the threshold.

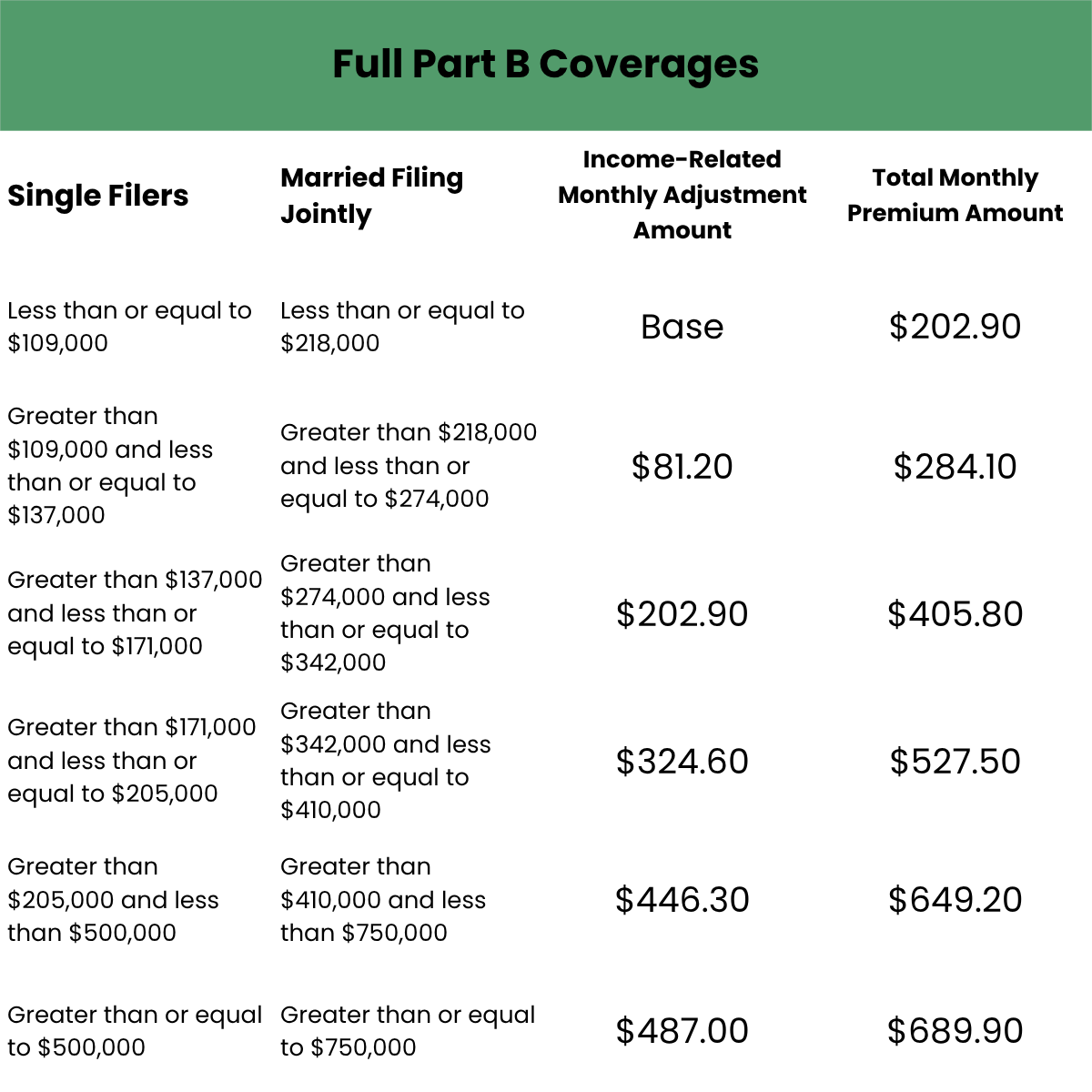

The 2026 IRMAA Brackets

Here's what the surcharge looks like this year, for most Medicare beneficiaries:

Source: Centers for Medicare & Medicaid Services, 2026. Part D surcharges are additional.

Notice something about that table: the surcharge jumps in big, sudden steps — not a gradual slope. Earn one dollar over the $109,000 line as a single filer, and your Medicare bill jumps by over $80 a month. That's what's called a cliff, and it catches a lot of people off guard.

For a married couple, both on Medicare, a single dollar over the threshold can cost both spouses the surcharge — potentially adding $2,000 or more to your annual healthcare expenses.

Who's Most at Risk — and Why

You might be thinking, "I don't earn that much." But IRMAA isn't just about salary. Your MAGI includes:

Wages and self-employment income

Required Minimum Distributions (RMDs) from your IRA or 401(k)

Social Security benefits (up to 85% is taxable)

Capital gains from selling investments or property

Roth conversions — a big one for people doing gap-year tax planning

Rental income and pension payments

A retired couple living comfortably on $80,000 a year can suddenly find themselves in IRMAA territory because they took a larger-than-normal IRA withdrawal, sold a rental property, or did a Roth conversion to take advantage of lower tax rates. The income bump is temporary. The Medicare surcharge lasts the entire year — and potentially the next year, too.

Five Things You Can Do Right Now

If you're still a few years from Medicare, you have real options:

1. Know your projected MAGI for the two years before you turn 65. Your income in those years will set your Medicare premiums for your first two years on Medicare. A retirement planner can model this for you.

2. Be strategic about Roth conversions. Converting pre-tax IRA money to a Roth IRA in lower-income years is a popular strategy — but large conversions can push you over an IRMAA threshold. The math needs to work in both directions.

3. Time one-time income events carefully. If you're planning to sell investment property, exercise stock options, or take a large distribution, the year you do it has Medicare consequences two years out.

4. Coordinate capital gains harvesting with IRMAA brackets. Taking capital gains in years when your income is low (early retirement, before Social Security starts) may keep you under the threshold.

5. Consider Qualified Charitable Distributions (QCDs). If you're 70½ or older, donating directly from your IRA to charity — up to $111,000 in 2026 — keeps that money out of your MAGI entirely, which can reduce or eliminate your IRMAA exposure.

Already On Medicare and Got Surprised? You Can Appeal

If your income dropped significantly — because you retired, lost a spouse, or experienced another major life change — you don't have to simply accept the higher premium.

The Social Security Administration allows you to appeal IRMAA using Form SSA-44. If you retired in 2024 or 2025 and your 2026 premiums are based on a high-income year that no longer reflects your situation, you may be able to request a reassessment using more recent income data.

This is one of the most underused tools in retirement planning — and it can eliminate a surcharge entirely.

The Bigger Picture

IRMAA is one of several places where income in retirement has compounding consequences: higher Medicare premiums, a larger share of Social Security being taxed, potentially higher income taxes. These effects don't always show up in simple retirement calculators, which is exactly why it helps to look at the full picture before decisions get locked in.

The good news: most IRMAA surprises are preventable with a little advance planning. The window for doing that planning is wider than most people realize — and you don't have to figure it out alone.

If you'd like a second set of eyes on how your income plan might interact with Medicare premiums, Adam Elesie offers a no-obligation conversation. Reach out here.

Disclosure: This article is for educational purposes only and does not constitute tax, legal, or investment advice. Individual circumstances vary — please consult a qualified professional before making planning decisions.