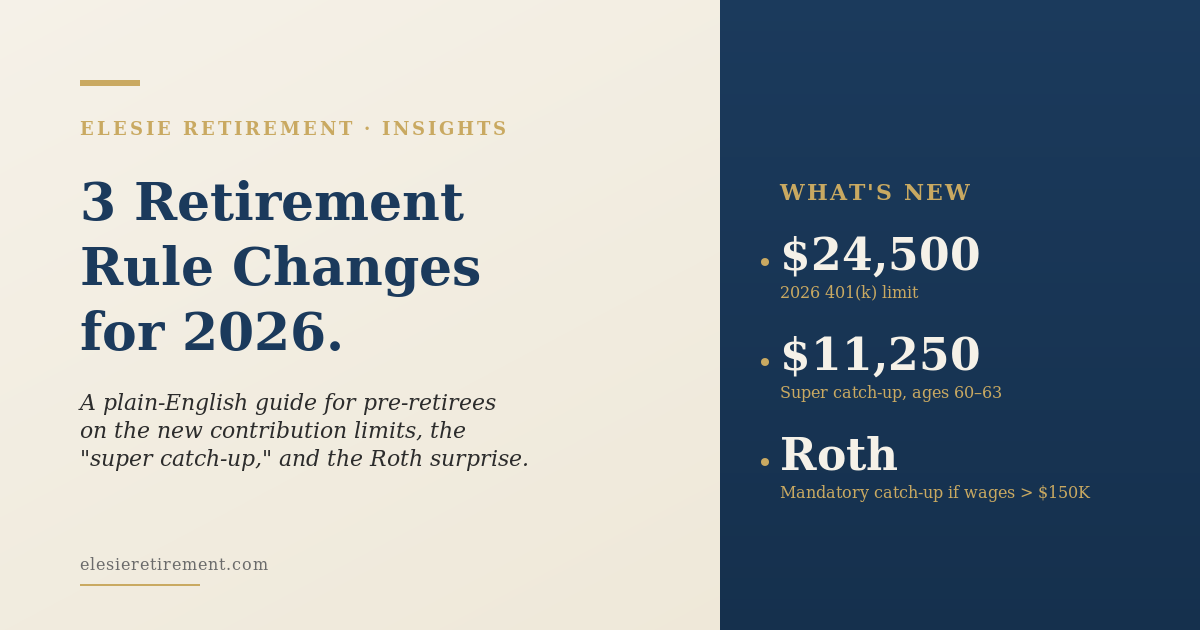

The Three 2026 Retirement Rule Changes Every Pre-Retiree Should Know About

If you're somewhere in the runway between 55 and 65, the years right before retirement do a lot of heavy lifting. They're often your highest-earning years. They're the last chance to top off accounts you've been building for decades. And they're the years when small adjustments, made quietly and consistently, can shape what the next thirty years actually feel like.

Three things changed in January 2026 that pre-retirees should know about. None of them are dramatic on the surface. All of them can quietly add thousands of dollars to your eventual income — or, if you ignore them, quietly cost you.

Here's what shifted, and what to actually do about it.

1. The contribution limits went up — and most people will leave the increase on the table

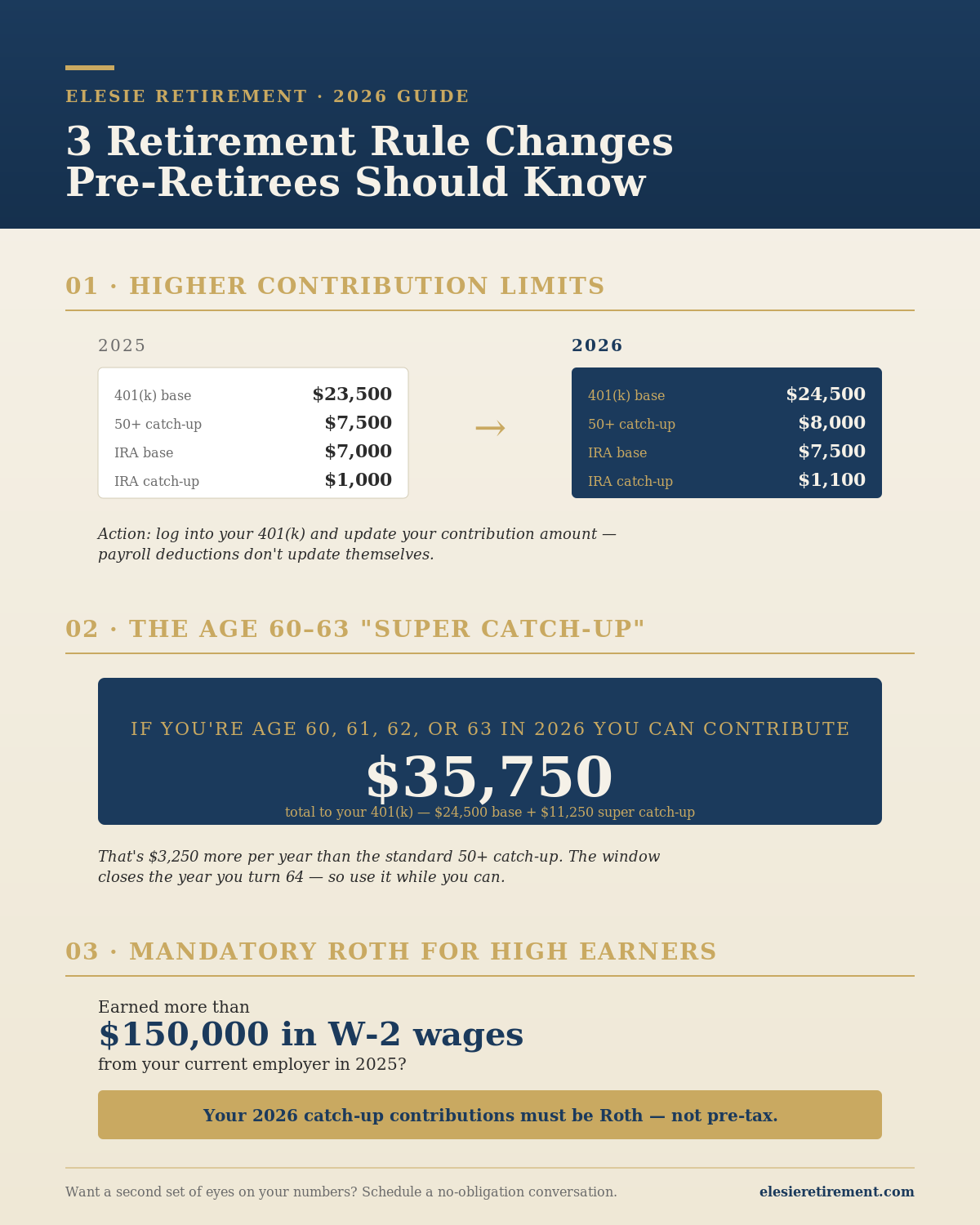

The IRS raised the standard 401(k) contribution limit to $24,500 for 2026, up from $23,500 in 2025. The IRA limit moved to $7,500, up from $7,000.

If you're 50 or older, you can also make a catch-up contribution. That number is now $8,000 in your 401(k) (up from $7,500) and $1,100 in your IRA. Stacked together, a saver age 50+ can put away $32,500 in a 401(k) plus $8,600 in an IRA in 2026.

That's a meaningful jump from last year. But here's the part most savers miss: payroll deductions don't update themselves. Your contribution percentage from December may still be sitting in your account today, capping you at last year's number. A two-minute login to your plan's website is often the difference between maxing out the new limit and leaving roughly $1,000 of tax-advantaged room unused this year.

What to do: Log into your 401(k) and confirm your contribution amount or percentage is set to hit the new $24,500 (or $32,500 if you're 50+). If you front-load contributions early in the year, double-check the math so you don't accidentally miss the employer match in later months.

2. The "super catch-up" for ages 60 to 63 is the most under-used rule on the books

This one is quieter and, for the right person, the most valuable.

Under SECURE Act 2.0, savers ages 60, 61, 62, and 63 are eligible for an enhanced catch-up contribution. In 2026, that limit is $11,250 — significantly higher than the standard $8,000 catch-up available to everyone 50+.

For someone in that four-year window, the math looks like this:

Standard 401(k) limit: $24,500

Super catch-up (age 60-63): $11,250

Total possible 401(k) contribution: $35,750

That's an extra $3,250 per year above the standard 50+ catch-up — and it's available for four full years. Across that window, a couple where both spouses are in the 60-63 band could move an additional $26,000 into tax-advantaged accounts. For households at the top of their earning curve, that translates to real dollars at real tax rates — often the difference between paying tax on that money now at 24% or 32%, versus letting it grow tax-deferred for years.

Two things to know:

The window is fixed. Once you turn 64, you drop back to the standard $8,000 catch-up — even if you keep working.

Not every employer plan has updated its systems to support the higher limit yet. If your plan provider hasn't enabled it, you can usually push them to — or, in the meantime, route the difference into an IRA.

What to do: If you're 60 to 63 (or your spouse is), check whether your plan supports the super catch-up. If it does, raise your contribution. If it doesn't, ask why — and ask when.

3. The Roth catch-up rule is now mandatory for high earners — and it changes your tax math

This is the change that's tripping people up.

Starting in 2026, if you earned more than $150,000 in wages from your current employer in 2025, your catch-up contributions can no longer go into a traditional, pre-tax 401(k). They must be made on a Roth basis — meaning you pay income tax on them now, and they grow tax-free forever after.

A few things worth saying clearly:

This applies only to the catch-up portion (the extra $8,000 or $11,250). Your regular contribution can still go pre-tax.

The income test is based on FICA wages from the prior year at your current employer. It is not based on your overall household income, your spouse's income, or self-employment income. If you switched jobs in 2025, the count resets.

If your plan does not yet offer a Roth option, the IRS allowed a transition period — but most providers have now built it out.

For a saver in a high tax bracket, this can feel like a step backward. You're losing the immediate tax deduction on $8,000 to $11,250 of contributions. But there's a quieter upside: you're now building a meaningful Roth balance that will never be taxed again, won't trigger required minimum distributions, and can pass to heirs tax-free. Over a 20- or 30-year retirement, the math often works out in your favor.

What to do: If you're a high earner using catch-ups, decide before your next paycheck whether you want to keep contributing the same dollar amount (which now lands as Roth and slightly reduces take-home pay) or adjust. Either way, also revisit your overall pre-tax versus Roth mix — this rule may be the nudge to look at Roth conversions in the gap years between retiring and starting Social Security or Medicare.

The bigger picture

The 2026 changes aren't earth-shattering on their own. But they're a useful reminder that the rules around retirement accounts shift quietly almost every year, and the gap between people who notice and people who don't is rarely about intelligence — it's about who has someone looking over the strategy with them.

The savers who do best in this stretch tend to share three habits: they update their contributions every January, they think two and three years ahead about their tax brackets, and they ask "what changed?" when a new year starts.

If any of the three rules above apply to you and you're not sure how to make the most of them, that's a conversation worth having before your next paycheck cycle. We'd be happy to be a second set of eyes on your numbers — no obligation, no sales pitch, just a clear look at what these changes mean for your plan.

Adam Elesie is a Certified Financial Fiduciary® and the founder of Elesie Retirement, a fee-conscious planning firm focused on helping pre-retirees and retirees connect every part of their financial life — income, taxes, Social Security, Medicare, and estate — into one clear strategy.

This article is for educational purposes only and does not constitute tax, legal, or investment advice. Contribution limits and tax rules are based on IRS and SSA guidance as of May 2026 and may change. Please consult a qualified professional about your specific situation.