The Health Insurance Gap: How to Cover Yourself Between Early Retirement and Medicare

For a lot of folks I sit down with, the dream is to step away from work a few years early…maybe at 60, maybe at 62… and finally enjoy the time they've worked so hard for. Then the same question stops them cold every time: "But what do I do about health insurance until Medicare kicks in at 65?"

It's one of the biggest, most underestimated hurdles standing between people and an earlier retirement. The years between your last day of work and your 65th birthday are what I call the health insurance gap and the price of crossing it just went up in 2026. The good news is that with a little planning, this gap is very bridgeable. Let's walk through it together.

The Quiet Tax Window in Your 60s….. And Why Most Pre-Retirees Miss It

There's a stretch of years in most people's retirement that almost nobody talks about at the kitchen table. It usually opens the moment you stop drawing a paycheck and closes the year you turn 73, when Uncle Sam taps you on the shoulder and reminds you it's time to start pulling money out of your IRA whether you need it or not.

We call it the gap years. And for a lot of pre-retirees I sit down with, it turns out to be the best tax planning opportunity of their entire lives — if they know it's there.

Should You Claim Social Security at 62, 67, or 70? Plain-English Math for Pre-Retirees

It might be the most expensive button you ever push. Once you tell Social Security when to start your benefit, that decision locks in for the rest of your life. There's a narrow 12-month window to undo it, but for most retirees the choice is permanent — and depending on which doorway you walk through, the difference can add up to six figures over a long retirement. So let's slow down and walk through it together, the way I'd talk it over with a friend at the kitchen table.

The Medicare Premium Surprise Most Pre-Retirees Don't See Coming

Imagine this: you've worked for decades, saved carefully, and finally handed in your badge. Medicare kicks in at 65, and you're feeling good about your plan. Then the first bill arrives — and it's $200 or $300 more per month than the standard premium you'd been counting on.

No mistake. No glitch. Just a rule that most people have never heard of, quietly doing exactly what it was designed to do.

That rule has a name: IRMAA — the Income-Related Monthly Adjustment Amount. And if you're between 55 and 65, understanding it now could save you thousands of dollars and a very unpleasant surprise.

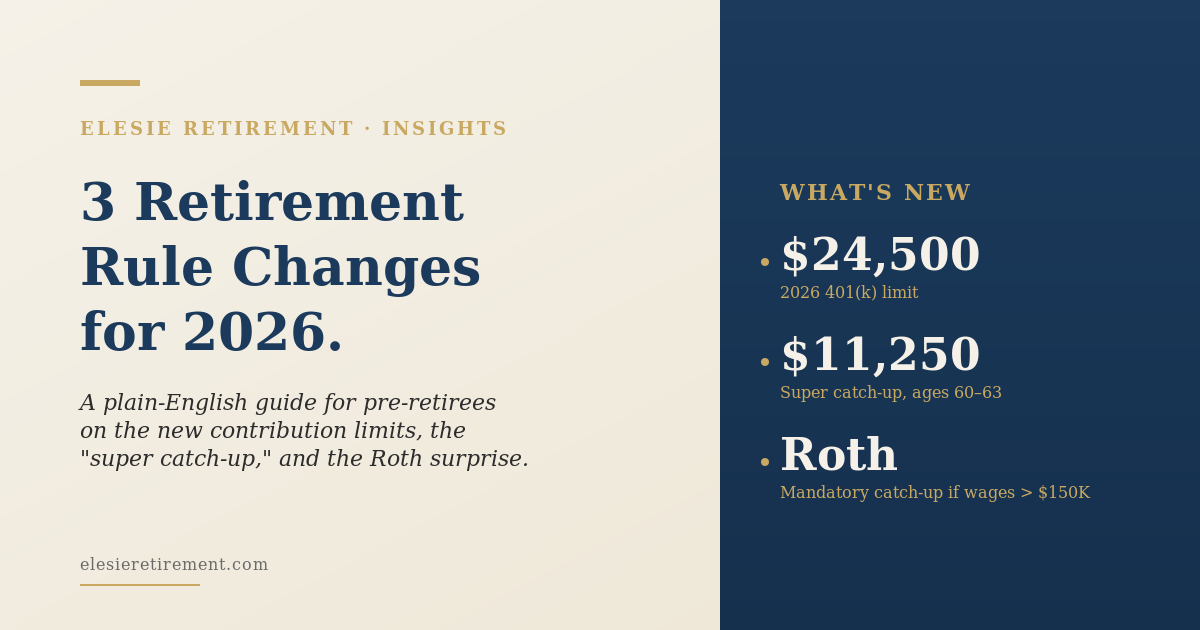

The Three 2026 Retirement Rule Changes Every Pre-Retiree Should Know About

A plain-English guide to the new contribution limits in 2026 for retirees, the under-the-radar "super catch-up," and the Roth surprise that's catching high earners off guard.

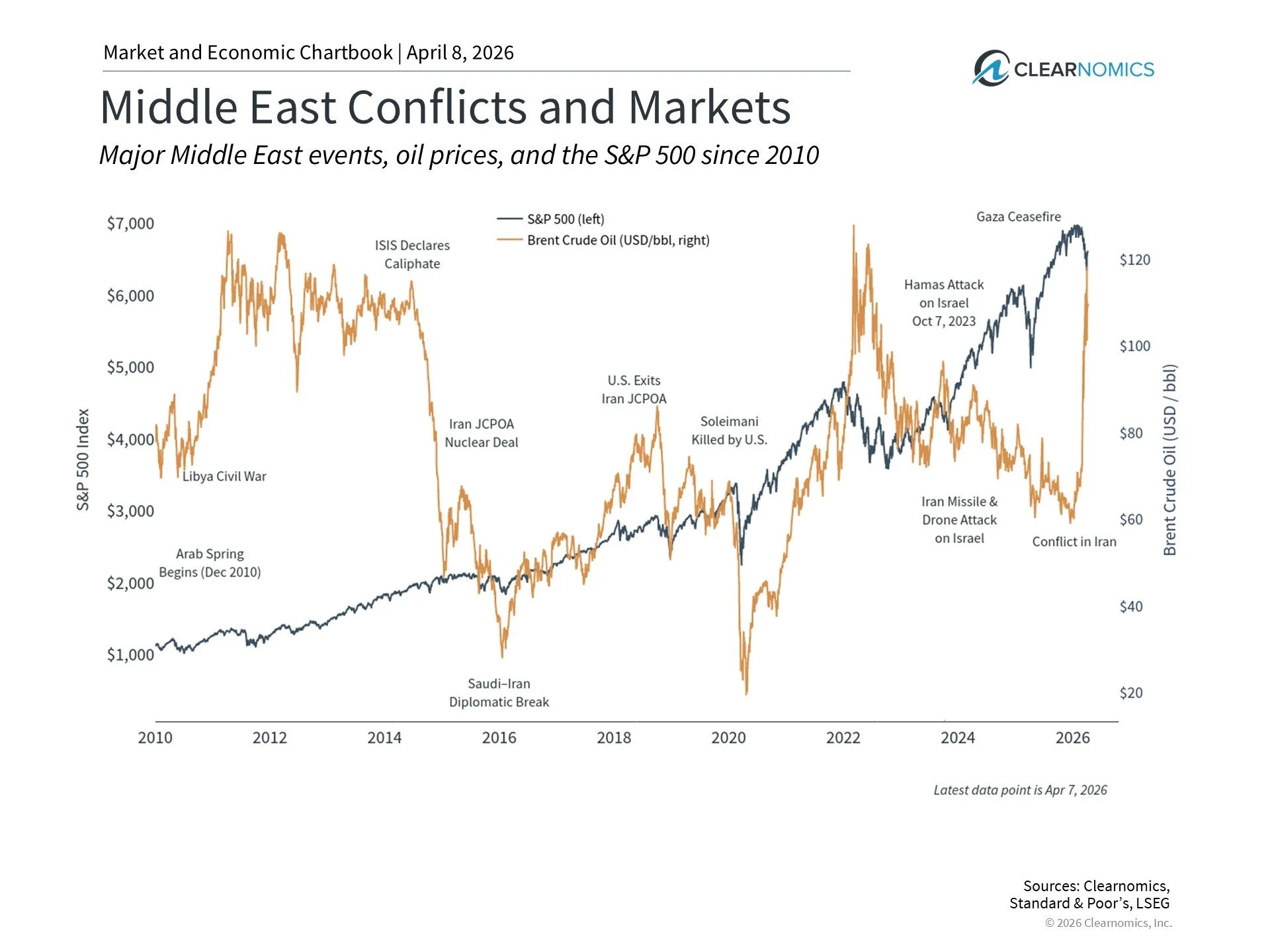

When Headlines Move Markets: What the Iran Ceasefire Really Means for Investors

In the wake of a recently announced two-week ceasefire between the United States and Iran, financial markets reacted immediately. Oil prices dropped sharply. Stocks rebounded. For a moment, a period of heightened geopolitical tension appeared to ease.

But beneath the surface, the story is more nuanced and far more instructive for long-term investors.

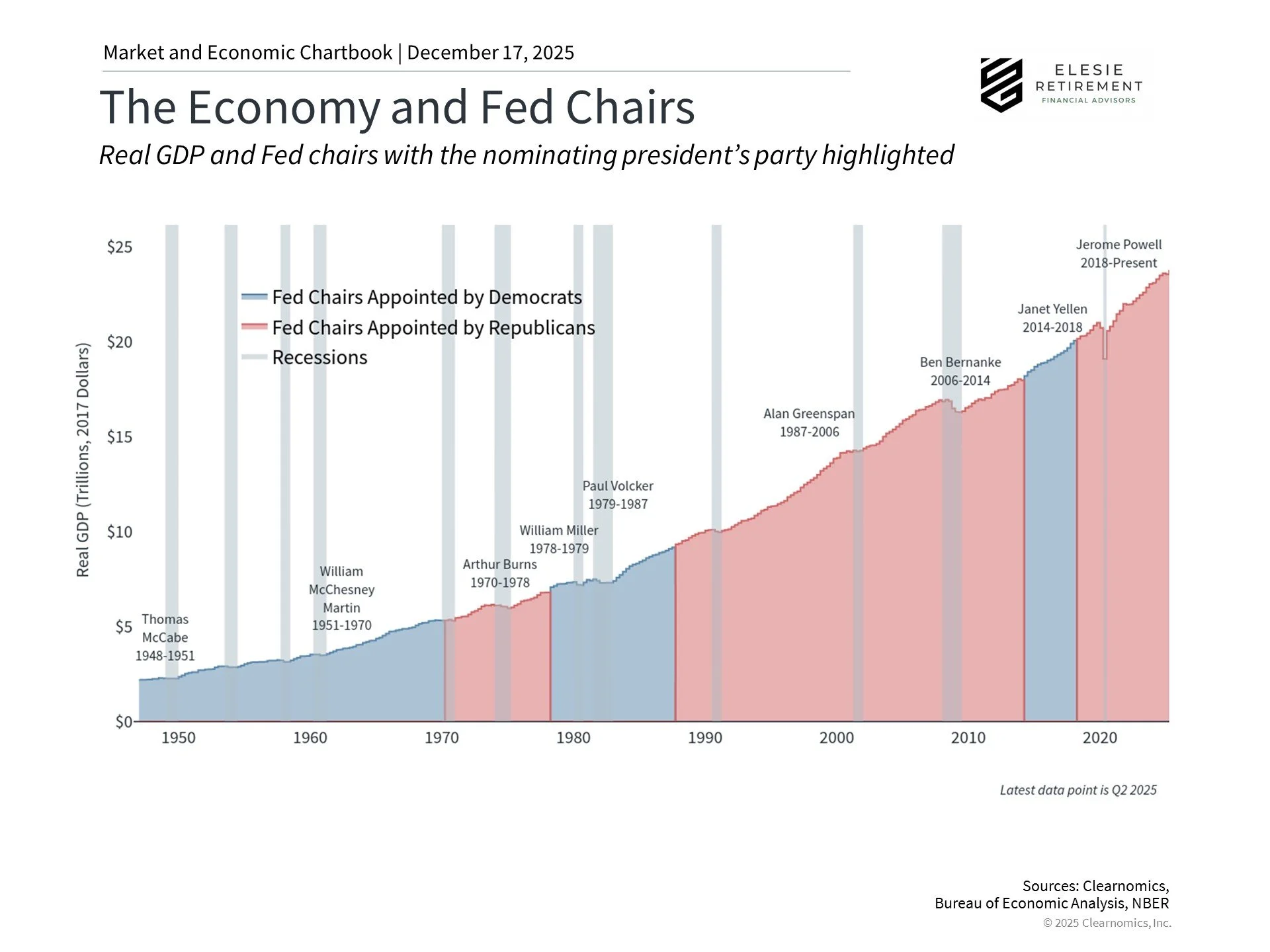

What's Next for the Federal Reserve: New Leadership and Interest Rates

The Federal Reserve—often called "the Fed"—is very important for investors who are saving for the long term. The Fed helps keep the economy and financial system running smoothly. In 2026, the Fed will be especially important because Jerome Powell's time as Fed Chair ends in May. This means the White House will choose a new leader for the Fed, which could change how the Fed makes decisions. These changes could affect interest rates, the stock market, and your investments.

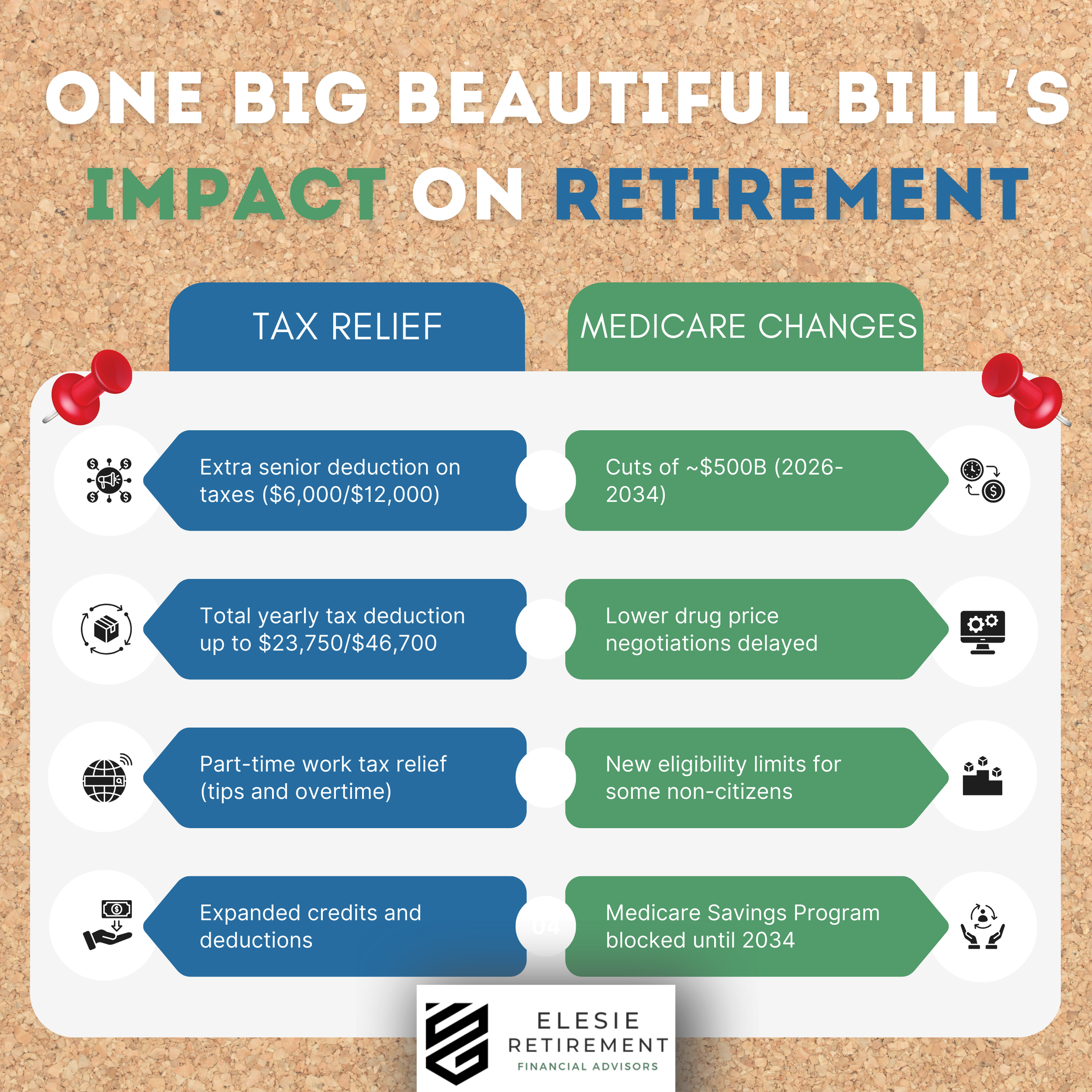

The One Big Beautiful Bill and What It Means for Your Retirement

The One Big Beautiful Bill Act of 2025 reshapes retirement planning in America. Seniors may benefit from larger standard deductions, expanded SALT cap relief, and new tax breaks for part-time work. Yet the law also introduces challenges, including $500 billion in Medicare cuts, delayed drug price negotiations, and limits on Medicare Savings Programs. Learn what these changes mean for Social Security, healthcare costs, and long-term financial security — and how to adjust your retirement strategy to make the most of today’s relief while preparing for tomorrow’s uncertainty.