The Fragile Decade: Why the Five Years Around Retirement Matter Most

Here's a question I ask a lot of the folks who sit down across from me: If the market dropped 20% the year you retired, would your plan survive it?

Most people pause. They've spent thirty or forty years watching their 401(k) go up and down, and they've learned — rightly — not to panic when it dips. A bad year in your forties barely leaves a mark. You weren't touching the money, so it had time to recover, and it always did.

But something changes the moment you stop earning a paycheck and start living off your savings. That same 20% drop, in that same account, can do damage that never fully heals. Not because the math of investing changed — but because your relationship to it did.

This is the risk almost nobody warns you about. It has a clunky name — sequence-of-returns risk — but the idea underneath it is simple, and it's one of the most important things a pre-retiree can understand. So let's walk through it together, the way I would at my kitchen table.

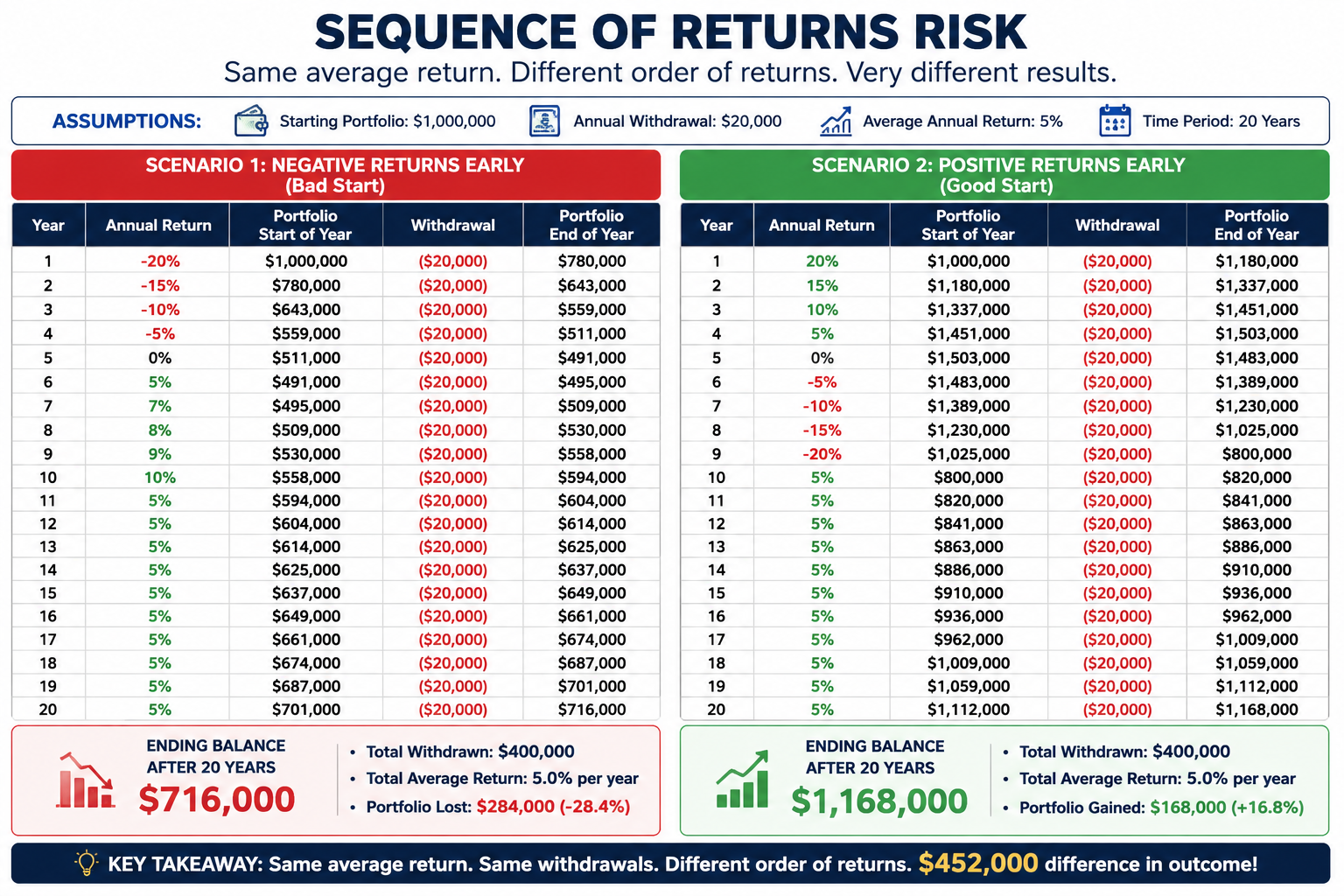

The same average, two very different endings

Imagine two people, Carol and Dave. Both retire with the same nest egg. Both draw the same amount each year to live on. And over their retirements, both earn the exact same average return.

You'd think they'd end up in the same place. They don't — and it's not close.

The difference is the order the returns show up in. Carol hits a rough market in her first few years of retirement. Because she's withdrawing money to pay her bills, she has to sell investments while they're down — locking in those losses and leaving fewer shares to grow when the market recovers. Dave, by pure luck, gets his good years first. His portfolio grows early, so when the bad years finally come, he's drawing from a much bigger, sturdier balance.

Same average return. Same withdrawals. One of them can run short a decade early, and the other dies with money to spare. The only thing that separated them was timing — something neither of them could control.

That's sequence-of-returns risk in a nutshell: when your bad years happen matters far more than most people realize, and the most dangerous time for a bad year is right at the start.

Why the timing hurts more once you retire

While you're working and saving, a market drop is almost a gift. You're still adding money every payday, so you're buying more shares at lower prices. Time is on your side.

Retirement flips that upside down. Now you're taking money out, not putting it in. When you sell during a downturn to cover your groceries and property taxes, those dollars are gone — they can't be there to rebound when the market climbs back. Researchers call the years right around your retirement date the “fragile decade” — roughly the five years before and the five years after you stop working. It's the stretch where your balance is at its biggest and a bad sequence can do the most lasting harm.

And here's the part that makes this timely: markets have been bumpy in 2026. After strong gains in 2025, the major indexes gave a lot of it back earlier this year amid tariff worries and recession chatter. If you retired recently and have been drawing from a portfolio that dipped, your sequence clock has already started ticking. That's not a reason to panic — it's a reason to make sure your plan was built for exactly this.

The good news: this risk is very manageable

I never bring this up to scare people. I bring it up because, unlike a lot of retirement worries, sequence risk is something you can actually plan around. Here are the levers I walk clients through.

Keep a cash cushion — your “market timeout” fund. If you have one to three years of living expenses set aside in something safe and stable, you don't have to sell stocks in a down market. You spend from the cushion instead and give your investments time to recover. It's the single most powerful protection against a bad sequence, and it's beautifully simple.

Be flexible with your withdrawals. A plan that lets you trim spending a little in a rough year — skip the big trip, hold off on the new car — takes enormous pressure off your portfolio. You don't have to slash your lifestyle. Small, temporary adjustments early can make the difference between running short and running comfortably.

Right-size your risk as you approach the finish line. The all-stock portfolio that served you well at 45 may be carrying more risk than you want at 63. Easing into a mix that still grows but doesn't swing as violently can shrink the size of that first bad year. The current research suggests a starting withdrawal rate around 3.9% for a balanced portfolio — a useful gut-check against the old “just take 4%” rule of thumb.

Build an income floor. Social Security is, in a very real sense, a paycheck that never runs out and isn't at the mercy of the market. Coordinating when you claim it — and, for some folks, layering in other guaranteed income — means a chunk of your essential bills gets covered no matter what stocks are doing. That's peace of mind you can't buy on a chart.

The takeaway

The years right around your retirement date carry a weight the rest of your investing life simply doesn't. A rough market at 45 is background noise. The same rough market at 63, with withdrawals starting, can quietly reshape your whole retirement. But timing you can't control doesn't have to mean risk you can't manage. A cash cushion, a little flexibility, a sensible mix, and a solid income floor can turn a fragile decade into a sturdy one.

If you're somewhere in that five-years-out-to-five-years-in window, the best time to stress-test your plan is before the bad year, not during it.

If you'd like a second set of eyes on your own plan — to see how it might hold up if the market turned rough right when you retire — Adam Elesie offers a no-obligation conversation. No pressure, no jargon, just a straight look at where you stand. Adam is a Certified Financial Fiduciary®, which means his job is to put your interests first, plain and simple.