The Health Insurance Gap: How to Cover Yourself Between Early Retirement and Medicare

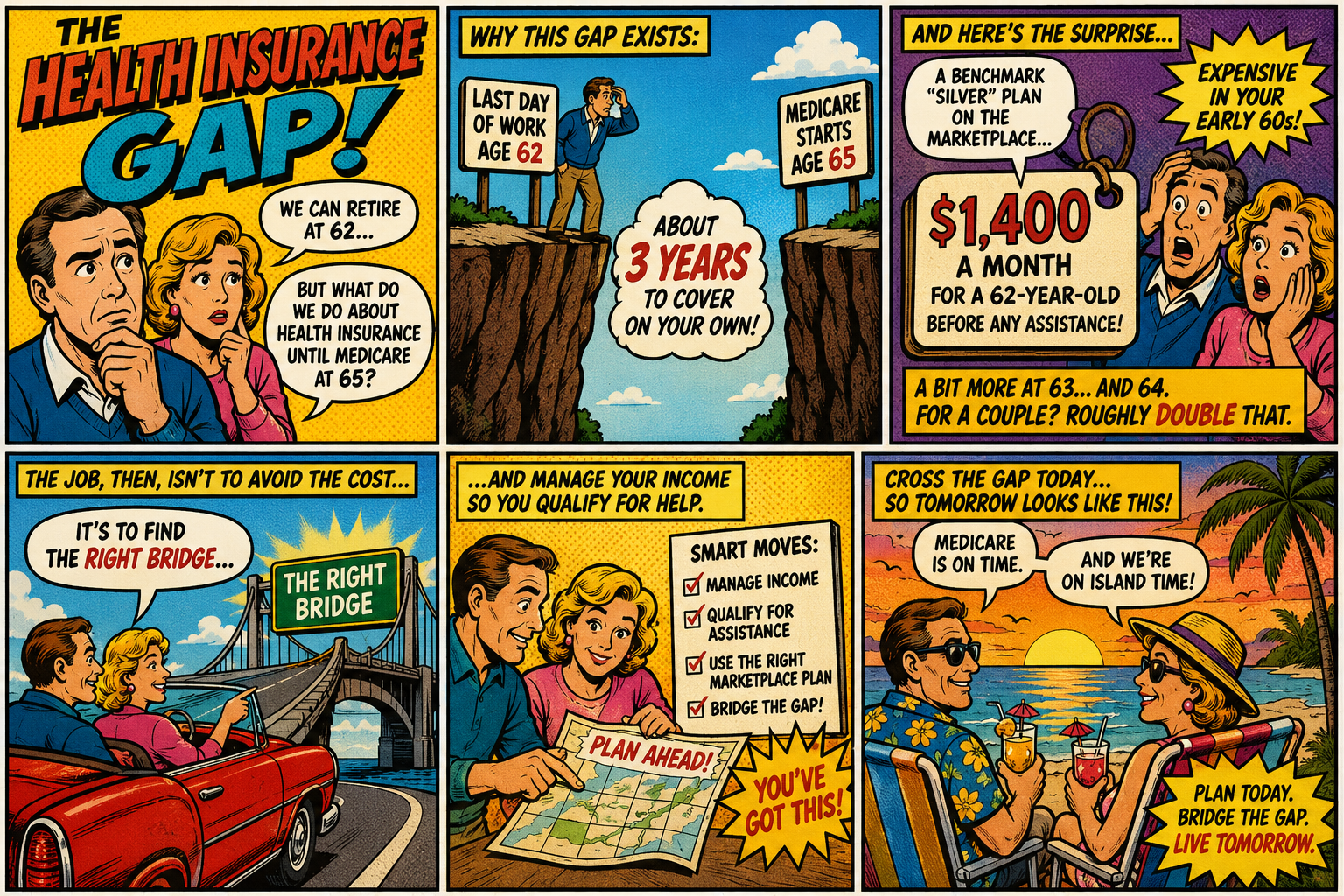

For a lot of folks I sit down with, the dream is to step away from work a few years early…maybe at 60, maybe at 62… and finally enjoy the time they've worked so hard for. Then the same question stops them cold every time: "But what do I do about health insurance until Medicare kicks in at 65?"

It's one of the biggest, most underestimated hurdles standing between people and an earlier retirement. The years between your last day of work and your 65th birthday are what I call the health insurance gap and the price of crossing it just went up in 2026. The good news is that with a little planning, this gap is very bridgeable. Let's walk through it together.

Why this gap exists

Medicare doesn't start until the month you turn 65 (with rare exceptions for certain disabilities). So if you retire at 62, you've got roughly three years to cover on your own — without the employer plan that's quietly paid most of your premiums your entire career.

And here's the part that surprises people: health insurance in your early 60s is genuinely expensive when you're buying it yourself. A benchmark "Silver" plan on the marketplace runs somewhere around $1,400 a month for a 62-year-old before any assistance — and a bit more at 63 and 64. For a couple, you can roughly double that. That's not a typo. It's simply what coverage costs at this age when no employer is footing part of the bill.

The job, then, isn't to avoid the cost. It's to find the right bridge and, just as importantly, to manage your income so you qualify for help.

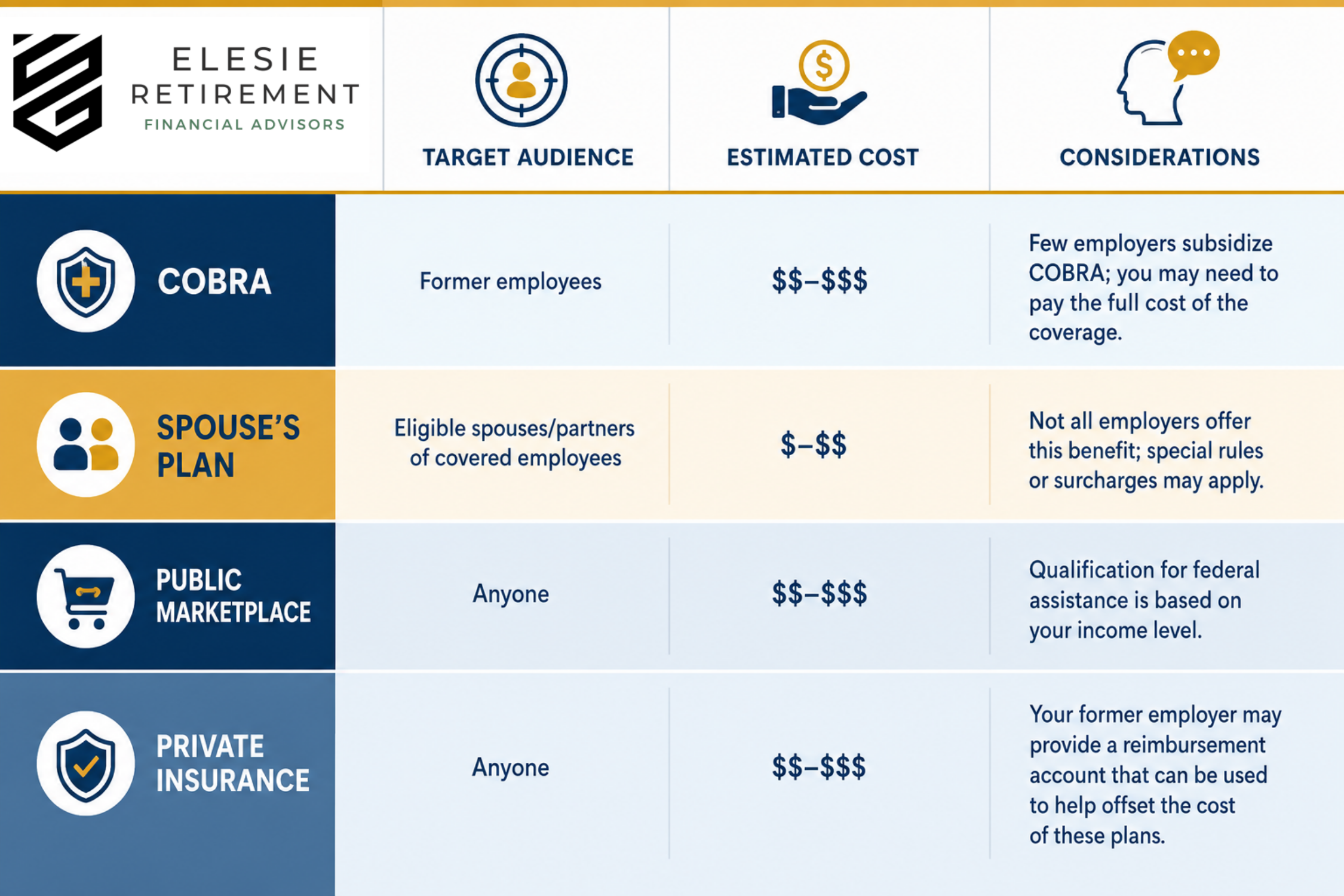

Your four main bridges

There's no single right answer here — the best path depends on your health, your spouse's situation, and your income. But almost everyone's options fall into one of four buckets.

1. COBRA — keep your old plan, for a while

When you leave a job, federal law usually lets you keep your employer's health plan for up to 18 months through a program called COBRA. The coverage is identical to what you had, which is comforting if you're mid-treatment or attached to your doctors.

The catch is the price. Your employer was likely paying a big share of that premium, and now you pay all of it — plus a 2% administrative fee. So a plan that cost you $250 a month as an employee might cost $700 or more on COBRA. For someone retiring at 63.5 or later, though, 18 months of COBRA can carry you neatly right up to Medicare. It's the simplest bridge when the timing lines up.

2. The ACA marketplace — and the comeback of the "subsidy cliff"

For most early retirees, the health insurance marketplace (healthcare.gov or your state's exchange) is the workhorse. You can't be turned down for pre-existing conditions, and depending on your income, the government may pay a meaningful chunk of your premium through a premium tax credit.

Here's the 2026 wrinkle you need to know about. For the past few years, a set of enhanced subsidies made marketplace coverage much more affordable for people across a wide range of incomes. Those enhanced credits expired at the end of 2025. Starting January 1, 2026, the old rules are back — and that means the return of something planners call the subsidy cliff.

The cliff works like this: if your household income lands above 400% of the federal poverty level, your premium tax credit doesn't shrink gradually — it disappears entirely. For 2026, that line sits at roughly $62,600 for a single person and $84,600 for a couple. Earn a dollar under it and you may get thousands in help. Earn a dollar over it and you could get nothing. That single dollar can be the difference between a $400 monthly premium and a $1,400 one.

I don't share that to scare you — I share it because it's one of the most controllable numbers in early retirement.

3. A spouse's plan

If your husband or wife is still working and has coverage at their job, the cleanest bridge may be hopping onto their plan. Leaving your own job typically counts as a "qualifying life event," which opens a special window to enroll outside the normal sign-up period. It's often far cheaper than COBRA or an unsubsidized marketplace plan — well worth a phone call to their HR department before you make any moves.

4. Part-time work with benefits

More employers than you'd think offer health benefits to part-time workers — think Costco, Starbucks, UPS, and many local outfits. A couple of shifts a week, doing something you actually enjoy, can solve the insurance problem and add a little structure to your early retirement. For some people this turns out to be the happiest bridge of all.

The income lever most people overlook

Here's where the planning gets interesting. When you're retired but not yet on Medicare, you often have real control over your taxable income. You decide how much to pull from your IRA, whether to convert money to a Roth this year, and when to realize gains in a brokerage account.

That control is power. Stay deliberately under that 400% poverty line and you may unlock substantial marketplace subsidies. But it cuts both ways — a large IRA withdrawal, a Roth conversion, or a big capital gain can quietly push you over the cliff and cost you your subsidy for the whole year. This is exactly why your health insurance plan and your tax plan can't live in separate drawers. They're the same conversation.

A simple way to start

If early retirement is on your mind, try this. First, count the months between your planned last day and the first day of the month you turn 65 — that's the gap you need to bridge. Second, estimate what your taxable income will realistically be in those years. Third, run your numbers through the official subsidy calculator at healthcare.gov, or your state exchange, to see where you'd land relative to that 400% line.

Those three steps will tell you, in an afternoon, whether your gap is a small step or a real leap — and which of the four bridges fits your situation best.

The years before Medicare don't have to be the thing that keeps you working longer than you want to. With a clear-eyed look at your options and a little coordination between your income and your coverage, this is a very solvable puzzle.

Adam Elesie - Certified Financial Fiduciary

If you'd like a second set of eyes on your own plan — including how your income choices might affect what you pay for health coverage before 65 — Adam offers a no-obligation conversation. Sometimes it just helps to talk it through with someone who does this every day.

This article is for general educational purposes and isn't tax, legal, or investment advice. Figures reflect 2026 rules and can change; please confirm the current numbers for your situation before acting.