The Quiet Tax Window in Your 60s….. And Why Most Pre-Retirees Miss It

There's a stretch of years in most people's retirement that almost nobody talks about at the kitchen table. It usually opens the moment you stop drawing a paycheck and closes the year you turn 73, when Uncle Sam taps you on the shoulder and reminds you it's time to start pulling money out of your IRA whether you need it or not.

We call it the gap years. And for a lot of pre-retirees I sit down with, it turns out to be the best tax planning opportunity of their entire lives — if they know it's there.

What's actually happening in the gap years

Picture a typical sixty-two-year-old who just retired. Their W-2 income has stopped. They haven't turned on Social Security yet — they're waiting until 67 or 70 to claim a bigger check. They're living off a savings account, maybe some brokerage dividends, while their IRA and 401(k) sit untouched.

For the IRS, that person has suddenly become someone with almost no taxable income.

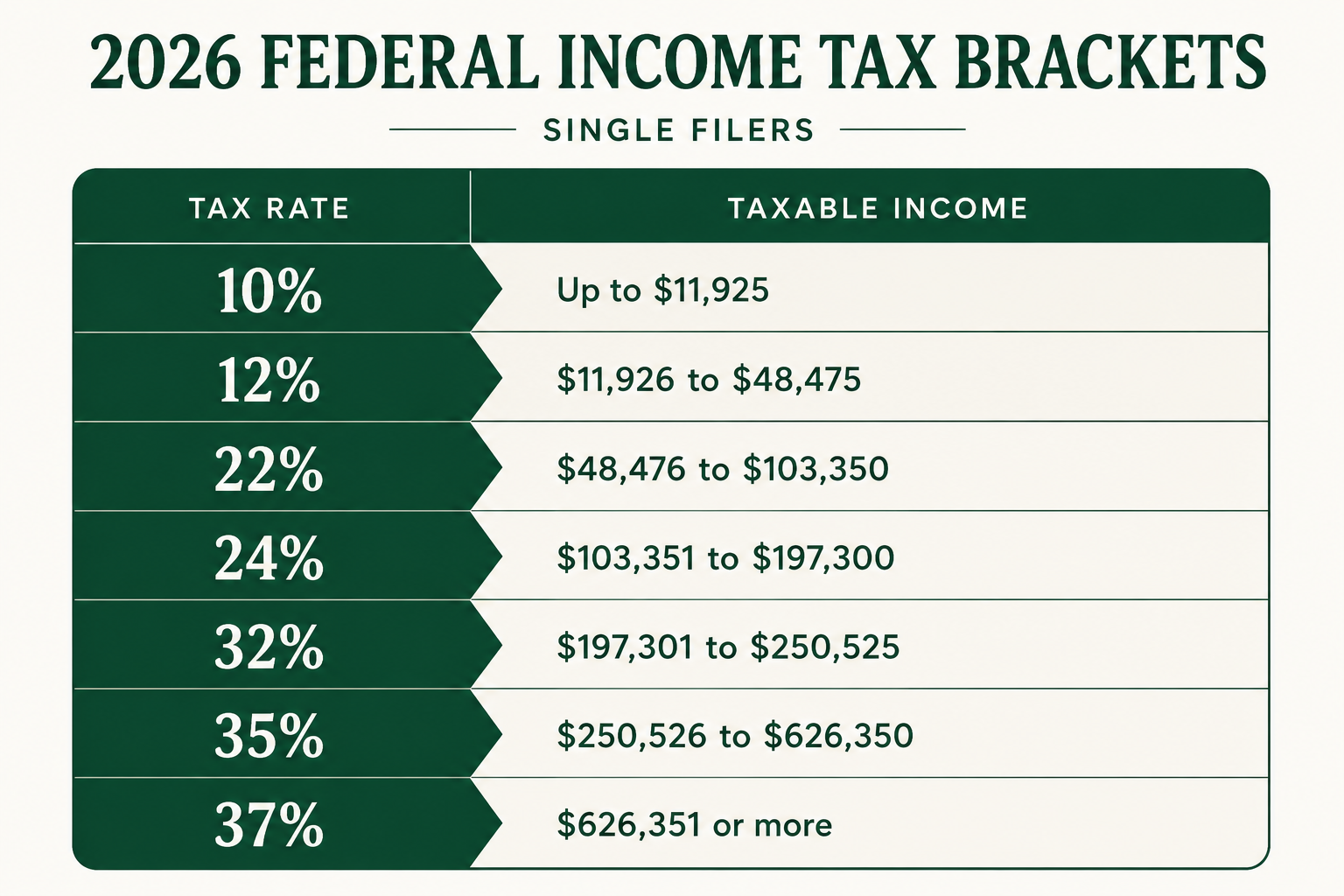

It feels strange to say it out loud, but a person who was in the 24% bracket the year before may now be in the 12% bracket — or even lower. And here's the thing nobody warns you about: that low-tax window is temporary. Once Social Security turns on, taxable income jumps. Once you hit age 73, Required Minimum Distributions kick in and force money out of your IRA each year, often pushing you right back into a higher bracket for the rest of your life.

So you have a handful of quiet years — sometimes just three or four, sometimes ten or more — where your tax bill is unusually low. The question is what to do with them.

The opportunity hiding in plain sight: the Roth conversion

A Roth conversion sounds technical, but the idea is plain. You take money out of your traditional IRA or 401(k), pay the income tax on it that year, and move it into a Roth IRA. From that point on, the money grows tax-free and comes out tax-free in retirement. There are no required withdrawals on a Roth, and your kids or grandkids can inherit it without an income tax hit.

In your working years, a conversion usually doesn't make sense — you'd be paying tax at your highest bracket. But in the gap years, when your taxable income has fallen off a cliff, the math flips. You can move chunks of money from "taxed later, when I'll probably be in a higher bracket" to "taxed now, while I'm in an unusually low one."

A couple I worked with recently — 64 and 65, freshly retired, sitting on a sizable IRA — converted about $90,000 a year for four years. That filled up the 12% bracket without spilling into 22%, and moved roughly $360,000 to the Roth side of the ledger at a marginal cost most retirees would dream of paying. Projected lifetime tax savings: well over $100,000.

The four guardrails I always check first

Roth conversions are powerful, but they aren't free, and they aren't right for everyone. Before I'd ever recommend one, here are the four things that have to line up.

One — your bracket today vs. your bracket later. If you'll genuinely be in a lower bracket once RMDs start, converting now usually doesn't help. But for most diligent savers — the kind of people who built up a strong IRA — the opposite is true. RMDs at 73 plus Social Security plus pension income often pushes them higher, not lower.

Two — where you'll pay the tax from. A conversion works best when you can pay the tax bill from a regular (taxable) savings or brokerage account, not from the IRA itself. Paying the tax out of the converted money is like driving with the parking brake on.

Three — IRMAA, that quiet Medicare surcharge. Once you turn 63, your tax return starts feeding into Medicare. Two years later, the IRS tells Medicare what you made, and if you crossed certain thresholds, your Part B and Part D premiums go up — sometimes by hundreds of dollars a month. A conversion that lifts your income $1 over an IRMAA cliff can wipe out a year of tax savings. We always model this before we hit the button.

Four — the five-year rule. Each conversion has its own five-year clock before you can pull out the earnings tax-free. For most pre-retirees this isn't a problem — but if you think you might tap that Roth money in the next few years, you need to plan around it.

"But I read that Roth conversions backfire for a lot of people"

You may have seen headlines warning that Roth conversions can come with a surprise tax bill. They can — if they're done sloppily. The usual culprits are: converting too much in a single year and jumping a bracket; ignoring IRMAA; forgetting to set aside cash for the tax; or converting at the wrong life stage. None of those are reasons to avoid the strategy. They're reasons to do it on purpose, with someone watching the dials.

The biggest mistake I see isn't converting too much. It's never converting at all — and then watching RMDs at 73 push someone into the 22% or 24% bracket for the rest of their life, when they had years of 12% bracket space sitting unused.

A short list of who should at least look at this

You don't need a financial planner to know whether this conversation is worth having. If most of these describe you, the gap years are probably your moment:

You're 58 to 70 and your retirement savings are mostly in traditional IRA or 401(k) accounts.

You expect a meaningful gap between when work income ends and when Social Security or RMDs begin.

You have some cash or taxable brokerage money to pay conversion taxes from.

You'd like to leave money to children or grandchildren, and you don't want them inheriting a tax bomb.

You're worried that tax rates will be higher in the future than they are now.

If two or three of those ring true, your gap years window is worth mapping out.

What to do this month

You don't have to decide anything today. But three small steps will put you ahead of almost everyone:

First, pull your most recent tax return and look at your taxable income line. Compare it to what you think it'll be the first year you're fully retired. That gap is your opportunity.

Second, write down the year you'll likely claim Social Security and the year you'll turn 73. Those bookend your gap years window.

Third, find out how much sits in traditional (pre-tax) accounts vs. Roth vs. taxable. Most people are surprised by how lopsided the picture is — and that imbalance is exactly what the gap years are designed to fix.

There's something deeply satisfying about a strategy that uses quiet years well. The gap years are short, they're easy to miss, and they only show up once. But for the pre-retirees who plan them on purpose, they can mean the difference between paying tax on your terms and paying it on the IRS's.

Adam Elesie is a Certified Financial Fiduciary® and the founder of Elesie Retirement. He helps everyday retirees in Long Beach and across the country build plans for income, taxes, Social Security, Medicare, and estate.

If you'd like a second set of eyes on your own plan — a quiet hour at the kitchen table, no obligation, just a look at your numbers — I'd be glad to sit down with you. That's what I'm here for.